Memo 1 - Clearview

Memo to: White Ink Investors

Re: Clearview

_____________________________________________________________________

The last two decades have seen wide spectrum technological advancement. Despite the positive progress we’ve made, investment decision making has gotten extremely convoluted due to one factor.

Noise.

Wall Street was always speculative, but the problem now is that this noise is so widespread that it has seeped down to everyone with a cellphone. There is now a constant frenzy in the stock market due to fast moving trends catalyzed by the development of a variety of trading platforms that have created a very casino like environment. Nobody seems to know what they are doing, merely riding the coattails of one another.

This is agonizing, confusing and most of all noisy.

Howard Marks in his 1995 memo quoted Tversky – a popular Stanford behaviorist.

“It’s frightening to think that you might not know something, but more frightening to think that, by and large, the world is run by people who have faith they know exactly what’s going on”

The world operates on decisions made in the noise, but to invest with noise is to speculate and to speculate is to gamble.

The question that stands in front of us now is – how can you drown out this noise to be able to pick the right stocks and avoid speculating? I’ve asked myself this question since I was 16.

Well, we can’t.

Rather, our focus should be singular – to find great businesses that are fundamentally strong, but momentarily underappreciated. We mustn’t care about what the market thinks about the business or its current share price but only it’s true intrinsic value.

We must note - noise doesn’t drive returns, but value, patience and discipline does - a CLEARVIEW does.

I started White Ink with this Clearview in mind: to craft a business where our bread-and-butter operation is to buy pieces of undervalued businesses and sell them when this undervaluation is corrected. Further, we aim to identify opportunities where profit is dependent on corporate action not market action.

But what do we do to have a Clearview?

We take the time-tested approach of value investing that has been perfected by the likes of Graham, Buffet and Munger and marry them with the principles of Shariah. I strongly believe deploying capital in high quality undervalued businesses within a risk-controlled environment while using Shariah investment principles as guardrails leads to an optimum Clearview.

But why Shariah?

Charlie Munger says “Good businesses are ethical businesses. A business model that relies on trickery is doomed to fail”. To me, there is no greater screen for identifying ethical businesses than Shariah principles.

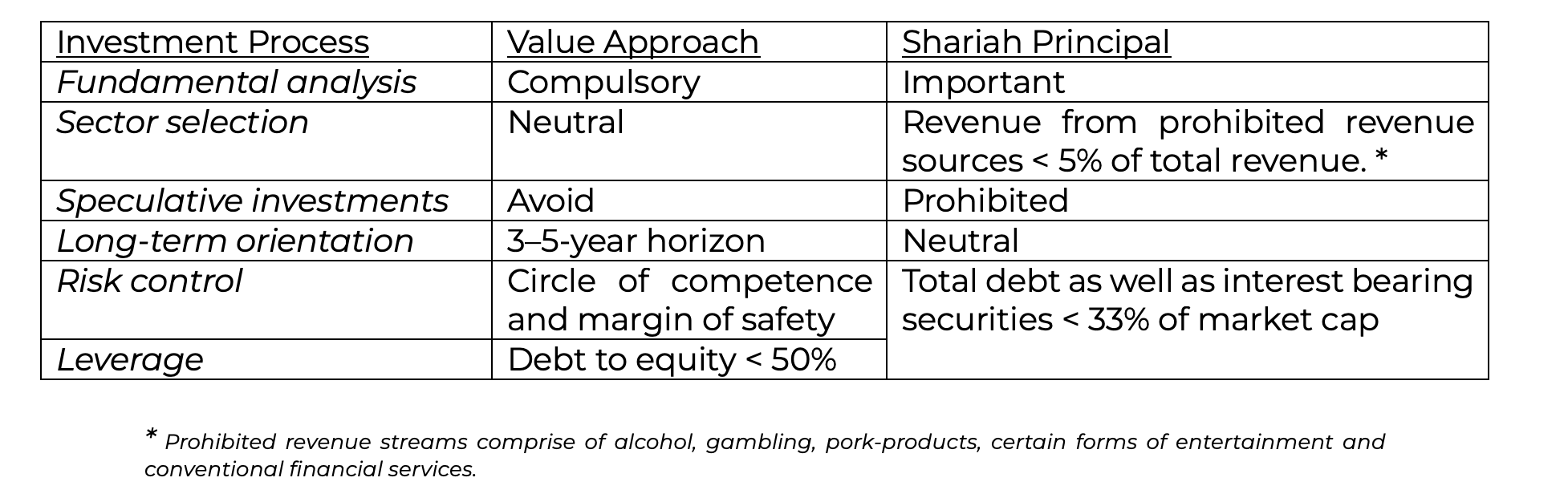

Now I must first point out that while the notion of merging value and shariah is new, their genetic makeup is quite similar, if not the same. Below, I have outlined how.

As you can see at many levels Shariah, and value investing align closely. But by formalizing and certifying this alignment I can open investment avenues for investors who are seeking ethical and responsible investments in underappreciated securities.

Our Method of Operation

“Value investors don't short stocks. Speculators short stocks. Value investors will engage in arbitrage and will have short positions that way, but value investors do not short. Value investors typically don't buy levered companies. Hedge funds have incentives to purchase levered assets” - Michael Price (MFP Investors) Lecture (A Discussion on Value Investing, at Fordham Law School -12/9/2015)

I believe this is in nutshell, what we do at White Ink.

Our avenues of investments can be broken down in two categories – Generals and workouts (forms of arbitrage).

1) General investments are long only positions in businesses that are trading below their true intrinsic value. This is assessed based on quantitative factors primarily, but a great deal of importance is given to qualitative factors as well. Our focus is to find a good bargain. We will make these investments by studying these businesses in great detail.

Here are some factors we look for while assessing value:

i) Economic moat

ii) Consistent and long-term quality management

iii) Free cash flow growth

iv) Price to free cash flow

v) 5-year ROI > 15%

vi) Price to earnings < 30

vii) Net margin > 15%

viii) High ROIC

2) Workouts are situations that arise from certain business and market activities – mergers, reorganizations, spin offs. These opportunities have a clear timeline and a known outcome, barring unforeseen issues. I would like to point out that I will never engage in a workout situation based on a run of the mill sort of rumor. I aim to only allocate capital in these situations once a public announcement has been issued. A workout is highly predictable and have a short holding period which could produce a decent annual rate of return. Since workouts rely on deal activity this will be a small (sometimes nil) but important portion of our portfolio. During a market decline, this category of capital allocation could help avoid broader market volatility preserving overall performance.

The most important point to note however is that all these businesses must FIRST pass our Shariah lens:

i) Non-compliant revenue must be < 5% of total revenue.

ii) Total debt to market cap < 33%

iii) Interest bearing securities to market cap < 33%

iv) Total of Cash, Deposits and Receivables to market cap < 70%

Our Shariah advisors, board and I will work hard to make sure all holdings remain Shariah compliant at all times – we have developed stringent controls, policies and review procedures for ensuring this.

Ground Rules

Here are a few axioms of utmost importance that I must emphasize on.

- I cannot promise fixed results to my partners. What I can and DO promise is that all investments will be made on the basis of value – we will steer clear of short-term trends at all costs as we are not in the business of chasing rainbows.

- We will at all times apply a risk-controlled approach to bring the risk of capital loss to an absolute minimum. Our aim is to always maintain a wide margin of safety, stay within our circle of competence and adhere to the Shariah investment tenets as our guardrails.

- I make no attempt to forecast the stock market or any business trends. I aim to search for value-driven growth. If you think such predictions are essential to an investment program – you should look elsewhere.

- The ‘Clearview Fund’ will be operated as if it were a holding company of sorts – our holdings just happen to trade in public markets. This long-term approach will help us foster the right temperament necessary for acquiring shares of great businesses.

With this in mind, I believe we have a great opportunity ahead of us.

If you have any questions – feel free to reach out.

Faithfully,

Zeeshaan W. Hakeem